May 30, 2018 Honorable Eric Garcetti, Mayor Honorable Michael Feuer, City Attorney Honorable Members of the Los Angeles City Council Re: Audit of the Systematic Code Enforcement Program of L.A.’s Multi-Residential Housing Stock

There is nothing more important than the safety and well-being of Angelenos. That is why my office undertook a review of the Systematic Code Enforcement Program (SCEP), which inspects the City’s residential rental units to verify compliance with state and local health, safety and building codes. This audit includes recommendations to streamline operations, work toward a more efficient system, and improve compliance so that all rental units within Los Angeles are safe and habitable.

Background: Created in 1998 to provide routine inspections of residential buildings with two or more rental units, SCEP inspections aim to curtail and remedy substandard Conditions.

Numbers: More than 96,000 properties and more than 740,000 rental units are subject to SCEP, which is conducted by the Los Angeles Housing and Community Investment Department (HCID).

How it works: Property owners are charged an annual fee for each rental unit to fund the inspection program. In addition to the proactive systematic inspections, HCID also administers a Complaint Inspection Program, which is a sub-component of SCEP, where inspectors conduct inspections of properties in response to a complaint that has been reported by a tenant or other person.

What’s working: HCID has:

Embraced the use of technology to identify and track code violations, and is upgrading its information systems to make it even more versatile;

Established a tiered inspection cycle whereby problematic buildings are to be inspected every two years instead of what had been a three-year inspection cycle. Buildings that have a track record of compliance are to be inspected every four years. My review found these approaches will help focus resources on the properties and units most in need of attention.

What can be improved: To improve SCEP’s fiscal processes, effectiveness and complaint response times, my audit recommends that HCID:

Respond more quickly to complaints to address response times that have lagged. HCID’s ability to respond to complaints within its goal of 72 hours fell from 89% in 2011 to 70% in 2017. This needs to be fixed.

Update HCID’s list of properties subject to SCEP to ensure inspections and billing are accurate. Currently, certain properties are erroneously inspected while others are incorrectly billed due to imprecise information.

Modernize the refund process that has not efficiently issued balances due back to property owners. In April 2017, more than 17,000 properties had credit balances of $2.9 million. Due to this audit, that number was whittled down to $1.9 million but HCID needs to do a better job of not wrongly billing – and notifying property owners proactively and timely if they are owed refunds.

Determine why Notices of Substandard Conditions (NSC) have drastically fallen despite an increase in violations. While the number of SCEP violations have increased since 2007, NSCs fell from 1,886 to 209 over the same ten-year period. Policymakers should be apprised of the reasons for the steep decline.

Why these recommendations matter: SCEP has helped to improve the habitability of housing in Los Angeles over the past two decades. That work must continue. With stronger financial oversight and more streamlined procedures, we can improve the quality, safety and condition of our City’s housing stock for the benefit of all.

Substandard, unsanitary, and deficient residential units have a direct impact on people’s quality of life – from lead and mold poisoning, to vermin infestations, to leaking roofs, shattered windows, and broken plumbing. To curtail and remedy these issues, the City enacted the Systematic Code Enforcement Program (SCEP) in 1998 within the former Los Angeles Housing Department, now the Housing and Community Investment Department (HCID)1.

By routinely inspecting buildings that have two or more rental units, SCEP is intended to protect the most basic need for safe housing for the City’s renters, including some of the City’s most vulnerable, low-income families.

To fund this work, HCID charges property owners a flat, annual fee for each unit that is rented in a multifamily building. The law allows property owners to pass this cost onto their tenants. Fee revenue collected by HCID is credited to a special revenue fund, known as the “Systematic Code Enforcement Trust Fund” #41M, managed by HCID. As actual program expenditures are incurred, primarily staffing and related costs paid by the City General Fund, HCID effects operating transfers from the special revenue fund to the General Fund.

While all of HCID’s multifamily residential code enforcement staff included 170 inspection and support staff, there were 61 SCEP inspectors assigned to conduct the proactive, cycle-based inspections of all rental units within the City. At the time of our audit, there were approximately 96,6002 properties representing 744,000 units subject to SCEP. Inspectors assess the units’ compliance with the City’s Building and Housing Codes by reviewing more than one hundred specific Code requirements (see Appendix II).

One SCEP cycle is defined as an inspection of all units within HCID’s inspection database. Originally, the City’s Housing Code required each unit to be inspected every three years; however, that cycle had not been met since the program’s inception, primarily because HCID lacked sufficient staff to complete the inspections within the three year period. In October 2016, HCID proposed a revised inspection cycle that considered its experience with inspection patterns, utilizing a risk-based approach. The modification was based on HCID’s evaluation of inspection data collected from several completed inspection cycles. It also considered prior Controller audits which emphasized the need to develop a risk-based approach to prioritize the inspections.

1 Prior to SCEP, general code enforcement of residential rental properties was the responsibility of the Department of Building and Safety.

2 While HCID sends bills for approximately 111,000 properties, many owners will apply for exemptions from SCEP fees and inspections.

In April 2017, the inspection cycle was modified to a two-tiered cycle: four years for compliant properties or two years for non-compliant/poorly maintained properties, to be implemented July 2018. Non-compliant properties were identified as having a history of multiple cited violations, complaints, and failure to resolve violations within the mandated timeframe.

The top code violations from the last complete inspection cycle (January 1, 2010 through June 30, 2014) were:

Fire Safety – Missing or defective smoke detectors

Maintenance – Defective or deteriorated plaster, drywall on walls or ceiling

Fire Safety – Missing or defective carbon monoxide detectors

Habitability – Missing, unsafe or defective floor coverings

In addition to the pro-active systematic inspections, HCID also administers the Complaint Inspection Program, which is a sub-component/program of SCEP. HCID inspectors conduct inspections of properties in response to a complaint that has been reported by a tenant or other person.Properties with violations that are not satisfactorily corrected can be referred to the Rent Escrow Account Program (REAP), which was established in 1988. REAP is an enforcement tool whereby tenants have the option to deposit rent owed to non-compliant owners into an escrow account set up by HCID until the owners correct the code violation.

Civil Grand Jury Report

On June 30, 2016 the County of Los Angeles Civil Grand Jury issued a report titled, “Renter or Landlord: Who Benefits?” related to the City’s SCEP and Rent Control programs. Regarding SCEP, the Grand Jury stated the following:

✓ Although required at least every three years, SCEP inspections of each rental unit had not been done every three years. HCID did not have sufficient staff to perform timely SCEP inspections or to perform inspections at each rental unit in the City every three years as required by the LAMC.

✓ HCID disseminated information to the public on SCEP and the Rent Stabilization Ordinance in Rent Stabilization Bulletins. However, the Bulletins omitted informing the public that SCEP inspections are required at least once every three years.

✓ The Systematic Code Enforcement Trust Fund had not been audited by the Controller in years.

The Grand Jury recommended that HCID should meet the three-year inspection requirement or amend the mandatory interval between inspections. In addition, the City Controller should be given sufficient funding to perform periodic audits of the Systematic Code Enforcement Trust Fund, and an audit of the Trust Fund should be done within three months.

Objective

This audit reviewed HCID’s activities and how SCEP helps to ensure that rental units remain compliant with the regulations in place intended to promote safe, healthy, and habitable housing for City renters. Accordingly, this audit reviewed financial and programmatic processes, and evaluated how Systematic Code Enforcement Trust Fund monies were accounted for and managed.

Favorable Conditions Noted

Based on our review of inspection processes, controls, and data, we found that SCEP activities generally identify rental units that met Housing Code requirements or did not comply with those requirements. Inspections identify violations related to general maintenance-type issues, as well as significant health or safety concerns, which are then classified as substandard3 rental units. While the number of HCID-classified substandard units at a given point in time fluctuates (as new units are identified and others have corrected the violations) it is noteworthy that as of November 2017, there were 867 units, within 99 properties, with an active Notice of Substandard Conditions. Also, since ninety percent of those had been issued within ten months, HCID indicated that owners with older violations had largely achieved compliance.

HCID uses technology to identify and track code violations in the field, with robust, internal databases. HCID also implemented recommended adjustments to SCEP, transitioning from an inspection cycle that examined all units once every three years, to a split inspection cycle that will re-examine problematic buildings every two years, and buildings that are generally code-compliant every four years.

Based on the new inspection cycle and past inspection efforts, it appears that HCID will be able to routinely inspect all properties subject to SCEP, but only if management is able to maintain its current staffing level of inspectors dedicated to this activity.

3 Substandard as defined by California Health and Safety Code Section 17920.3 are significant health or safety violations, such as lack of a working toilet, kitchen sink, lack of water, ventilation or heating, and structural hazards.

Areas Requiring Attention

Our audit determined that there were control gaps and procedural deficiencies with the HCID’s Billing and Collections Unit and Accounting Division that led to incorrect billing, inaccurate records, and delays in refunds for property owners.

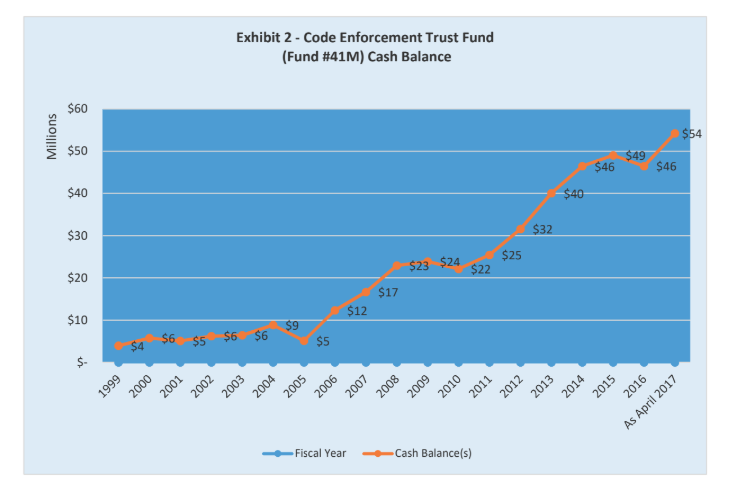

In the past, SCEP revenues exceeded the program’s costs. Although SCEP was operating on a three-year inspection cycle, it had fewer inspectors than anticipated (due to the City’s managed hiring freeze), and therefore did not perform every property inspection it should have within the necessary timeframe. The Department plans to initiate the Tier System in conjunction with the next inspection cycle projected to start in July 2018. Going forward, because it will switch to the two-tiered cycle, we anticipate that SCEP will have adequate staffing and resources will be fully utilized. Each inspector is responsible to inspect an average of 3,500 units per year. In the past, while all property owners and/or renters paid fees, SCEP did not inspect all units on schedule. This contributed to the Fund accumulating a high cash balance, $54 million as April 20174.

Accurately determining the full cost of the program and ensuring the fee structure reflects the work performed is important. Additional issues also impacted the Fund:

Imprecise information caused some properties to be billed and scheduled for inspection even though they were not subject to SCEP. These errors occurred because SCEP identifies subject properties based on a county database that tracks land use; however, land uses can change, (e.g. conversion from rented apartments to individually owned condos). Further, even if the county’s land use code is accurate, SCEP may not always apply; for example, a “home for the aged” in practice can be a senior assisted living facility which would not be subject to SCEP, or that same land code can refer to an age-restricted rental complex, which is subject to SCEP.

4 On June 28, 2017, the City Council authorized an emergency reserve SCEP fund equal to two months of operating costs in the event of a disaster occurring. $7.5 million was transferred from the unrestricted cash account to a restricted cash account within the Systematic Code Enforcement Trust Fund. The Fund’s cash balance as of December 2017 was $34 million.

We noted procedures that result in HCID inspecting and billing some property owners who should be exempt. A number of buildings have had the same SCEP-exempt uses for years. Despite the low likelihood that these uses will change, HCID management requires that many exemptions be renewed on a one or three-year basis. When these exemptions expire, the property returns to SCEP’s inspection inventory, bills are issued and inspectors are dispatched. Such procedures can erroneously bill property owners and waste inspector time.

An inadequate refund process makes it appear as though the Fund has more available money than it actually does. Currently, SCEP sends exemption applications and bills for fees at the same time. The result is that many building owners file for an exemption and pay their bill simultaneously, because they may be concerned that their application will be rejected and they will be penalized. However, when exemptions are approved, SCEP does not notify the owners that they have a credit, nor do they issue a refund unless an owner asks. As a result, some of the excess cash balance in the Fund is actually owed back to owners, who were exempted from paying these fees. As of April 2017, more than 17,000 properties had credit balances that totaled $2.9 million. Subsequent to fieldwork completion, we noted that HCID refunded $1.9 million of the $2.9 million in credit balances.

HCID’s ability to respond to complaints within its goal of 72 hours declined from 89% in 2011 to 70% in 2017. HCID also administers the Complaint Inspection Program whereby tenants or others may file complaints about rental properties. The Department’s goal is to contact the complainant within 72 hours. Due to a reduction in clerical staff, their response time has lagged. Also, while HCID monitors response time to complaints, there is no time-based goal for resolving complaints. The Department indicated that because scheduling inspections is dependent on the complainant’s availability, establishing a goal would be difficult.

What the Department should do next

To improve SCEP’s fiscal processes and complaint response times, HCID should:

Ensure that only properties subject to SCEP are billed for inspection fees, and questionable properties are adequately inventoried and reviewed by management;

Improve the exemption process and its timing so that exempt owners are not required to pay the fee, and properties that have been exempt for many years do not need to re-apply as frequently; and

Establish stronger controls to immediately refund property owners/tenants who were billed in error and subsequently paid.

Identify ways to address the need for more clerical support for the Complaint Inspection Program and monitor the actual results of complaint disposition timeliness, to evaluate the program and identify if corrective actions are necessary.

These and other findings and recommendations are discussed further in the detailed report.

Conclusion

SCEP has helped to improve the habitability of housing in Los Angeles through its identification and remediation of rental unit violations over the past two decades, and that work must continue. Stronger financial oversight and procedures are needed to make sure that SCEP’s budget and fee schedule accurately reflect its costs and the scope of its work. Such improvements will make sure tenants and owners continue to benefit from robust inspections, while paying for all appropriate costs.

Department Response & Action Plan

A draft of this report was provided to HCID management on January 19, 2018, and we met with Department management and representatives at an exit conference on February 13, 2018. While management generally agreed with the issues noted, we considered management’s views and comments as we finalized the report. HCID provided a formal response and action plan on March 6, 2018, which is included as Appendix III.

Based on our evaluation of the Department’s reported actions and implementation plan, we now consider 8 recommendations as Implemented (Recommendations 2.2, 2.3, 3.2, 3.3, 3.4, 4.1, 4.2, and 4.3); 6 In-Progress (Recommendations 1.1, 1.2, 3.1, 5.1, 6.1, and 7.1); and 1 as Not Yet Implemented (Recommendation 2.1). HCID disagreed with three recommendations (Recommendations A, 5.2 and 7.2).

We would like to thank HCID staff and management for their time and cooperation during this audit.

The 1997 Blue Ribbon Citizens’ Committee on Slum Housing (Blue Ribbon Committee) cited problems in Los Angeles based on the American Housing Survey for the Los Angeles- Long Beach Metropolitan Area, which noted more than 150,000 apartments that were substandard and in need of major repair. The Committee acknowledged the Metropolitan Area is larger than the City of Los Angeles but that the City had the great majority of rental housing in the Area.

In response to a Blue Ribbon Committee recommendation, the City established the Systematic Code Enforcement Program (SCEP) within the Los Angeles Housing Department, now known as the Housing and Community Investment Department (HCID). The purpose of SCEP is to proactively inspect multifamily residential rental properties to verify compliance with the standards set forth in the applicable building and housing codes. These codes help to ensure that all buildings, rental units and common areas of multifamily properties are safe and habitable, free of lead hazards, structural hazards, and sanitation problems. As of early 2017, there were approximately 96,600 rental properties with more than 744,000 units in the City that were subject to SCEP.

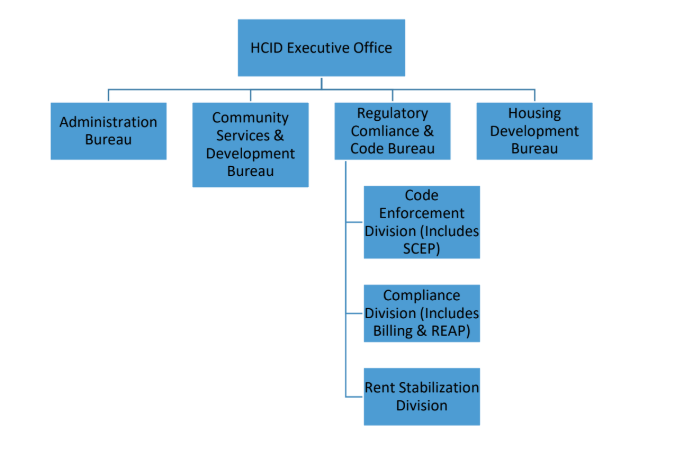

HCID and SCEP Operations

HCID facilitates the financing and development of affordable housing projects with business and community partners; oversees all City-funded housing programs to assist low-income populations, special needs populations and communities in general; makes renters aware of their rights; and helps ensure that landlords comply with the Rent Stabilization Ordinance and the City and State Housing Codes.

To carry out these responsibilities, HCID is organized into four Bureaus – Administration, Community Services and Development, Housing Development and Regulatory Compliance and Code. SCEP functions as part of the Code Enforcement Division, under the Regulatory Compliance and Code Bureau, as noted below.

SCEP operations are decentralized and located in five regional offices: North Valley, South Bay, East Los Angeles, West Los Angeles and Central (Wilshire District), as grouped by census tract. Each regional office has three inspection teams; each team is comprised of one supervising inspector, four SCEP inspectors, one complaint-response inspector, one assistant inspector, and one clerk.

Each region has very different property characteristics that the Department must consider in executing its inspection activities. For example, there are generally smaller properties in the South area that are individually owned and operated, while the Westside and Downtown areas have larger buildings that are commercially owned and managed. Further, factors such as limited neighborhood parking can impact the time it takes for inspectors to conduct their work.

Properties Subject to SCEP

HCID inspectors are responsible for inspecting thousands of multifamily properties / rental units. These counts are not static and change frequently due to new construction and demolition of units in the City. Keeping track of the properties/owner information is challenging due to the constant turnover of ownership. Therefore, HCID utilizes multiple databases to identify and track apartment buildings, duplexes, residential hotels, and other multifamily properties and their ownership. The primary source of property information is the County’s Property Tax Assessment database which includes all properties within the City identified by Assessor Parcel Number (APN).

Each property within the County’s database is defined by a land use code, which describes how the property or building is used (single-family home, commercial building, multi- family building, vacant land, etc.). HCID uses the land use code and unit count to determine which properties are subject to SCEP, and this data is uploaded to a separate property database (PROPdb). While the County’s data has hundreds of land use codes, only 57 are subject to SCEP.

Los Angeles Municipal Code (LAMC) Section 161.301 defines how SCEP applies or does not apply to the following types of properties:

As noted above, there are many different types of residential housing that are not subject to SCEP fees and the related proactive, cycle-based inspections for habitability by HCID. Some of these housing types may be proactively inspected by other entities or governmental agencies, while others are subject to complaint-based inspections by the City’s Department of Building and Safety. Policymakers should be apprised of the residential property types exempt from SCEP that are (or are not) inspected by other agencies to help ensure habitability, and consider that information for potential expansion of SCEP through amending the City’s housing code.

Recommendation

A. HCID management should submit a report to the City Council identifying which residential property types that are currently exempt from SCEP are monitored by other agencies. Council may then use that information as a basis for considering expansion of SCEP by amending the LAMC.

Inspection Process

SCEP staff refer to the inspection process as a “conveyor belt,” as there is constant activity and tasks are often handed from one inspector or team, to another. This process is described below:

✓ When a property is scheduled for inspection, clerical staff generate a Notice of Inspection (NOI) letter approximately 30 days prior to the inspection to inform the owner that inspectors will be visiting the units.

✓ 5-7 days prior to the inspection, inspection staff posts a Tenant Inspection Notice at the property to inform tenants of the time and date of the inspection. (They provide a 30-minute window to account for any traffic or parking issues Inspectors may have.)

✓ On the day of the inspection, an inspector checks all buildings, rental units, and common areas of the property to ensure that units are habitable and in a condition for the “occupation of human beings.”

✓ If no violations are observed, the inspection is complete and the Code Compliance and Rent Information System (CCRIS) is updated. No further action is required.

✓ If violations are identified, a written order describing the violation is mailed to the owner and a copy of the order is posted at the property. Property owners must correct all cited violation(s) by the date specified on the order, which is typically 30 days after inspection. If the violation relates to unsanitary/unsafe conditions (e.g., a “hoarding” situation), a citation may be issued to the tenant to correct.

✓ If a property has one or more violation(s) that are considered severe i.e., an inspector finds a significant health or safety violation(s) pursuant to California Health & Safety Code Section 17920.3, the property owner is issued a Notice of Substandard Condition (NSC). Examples of Health & Safety Code violations include lack of hot and cold running water; lack of adequate heating; broken, rotted, split, or buckled exterior wall coverings or roof coverings, etc. NSCs may be issued due to violations related to the building or any dwelling unit.

✓ After the order to comply date, an inspector conducts a re-inspection to verify compliance. Inspectors can provide an extension to the owner if they determine sufficient progress has been made to address the violations.

✓ If violations are corrected, the inspector closes the case and no further action is required.

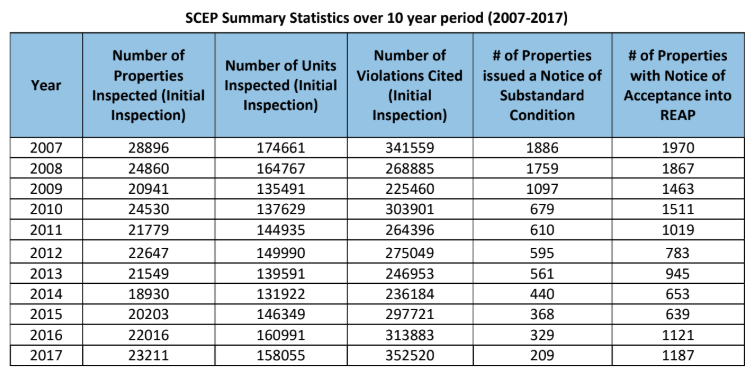

✓ If violations are not corrected, the property owner may have to pay re- inspection fees and may have to attend an administrative hearing, which may result in a referral to the City Attorney’s Office or placement in the City’s Rent Escrow Account Program (REAP). A Notice of Acceptance (NOA) into REAP is sent to the property owner, who may appeal the Department’s decision at a General Manager’s hearing. REAP encourages owners to make the repairs and return the property to a safe and habitable condition by reducing tenants’ rent and allowing them to pay into an escrow account, which is only available to the owner after HCID clears the building of all violations. As of October 31, 2016, there were 943 properties in REAP. While the majority of these were identified through HCID’s proactive, cycle-based inspections, 23% were identified by an inspection that was initiated by a complaint. Properties accepted into REAP may also be the result of NSCs that have not been corrected. HCID provided summary statistics related to SCEP inspections conducted5, violations cited6, properties issued a NSC, and properties with a NOA into REAP over a ten year period:

Note that the number of violations cited, and NSCs and NOAs issued, do not consider the timeliness of when (or if) owners made corrections to bring the properties into compliance; therefore, the data is not reflective of outstanding (uncorrected) issues.

Based on the summary statistics, the number of NSCs issued has decreased considerably over the ten-year period, although the number of violations cited has not. In addition, there is a wide variation in properties with a NOA into REAP, from a high of 1,970 and low of 639, a 68% difference. Policymakers should be apprised of the reasons for variation in numbers for NSCs and violations, as well as the more recent increase in NOAs issued.

5 The number of properties and units inspected noted are the initial SCEP inspection only; follow-up (re-inspections) to identify if corrections was made, and complaint based inspections are not included.

6 There are 131 potential violations for which a unit/property could be cited. Within HCID’s database, each violation is counted separately, regardless of severity or if multiple units within one property had the same issue. For example, if a 10-unit property included 8 units that were in full compliance, and one unit had 4 violations, and another unit had 6 violations, the property owner would be responsible for correcting 10 violations.

Recommendations:

B. HCID management should provide a report to the City Council, explaining why the number of Notices of Substandard Conditions has significantly declined although the number of violations cited has not.

C. HCID management should report to the City Council on its understanding of what accounts for the variability of properties issued a Notice of Acceptance into REAP, and specifically, the recent increase in the number compared to prior years.

Inspection Cycle

One SCEP cycle is defined as an inspection of all units within HCID’s inspection database. The City’s Housing Code previously required each multifamily unit to be inspected every three years. However, this inspection cycle had not been met since the inception of SCEP, primarily because the Department has not had sufficient staff to complete the inspections within three years. In October 2016, HCID proposed a revised inspection cycle that considered its experience with inspection patterns and utilizing a risk-based approach. The modification was based on HCID’s evaluation of inspection data collected over 18 years from several completed inspection cycles. It also considered prior Controller audits which emphasized the need to develop a risk-based approach to prioritize the inspections.

In April 2017, the inspection cycle was modified to a two-tiered cycle: four years for compliant properties or two years for non-compliant/poorly maintained properties. Non- compliant properties were identified as having a history of multiple cited violations, complaints, and failure to resolve violations within the mandated timeframe.

The next inspection cycle, based on the two-tiered approach, is projected to start in July 2018. Based on HCID’s data, 96% of the City’s rental housing properties will fall under a four-year inspection interval and about 4% will fall under a shortened, two-year inspection interval.

Based on the new inspection cycle and past inspection efforts, it appears that HCID will be able to inspect all the properties subject to SCEP within the expected timeframe, but only if it is able to maintain its current staffing level of inspectors. From 2010-2016, HCID had an average of 59 SCEP inspectors (51 field inspectors and 8 Assistant Inspectors). Each inspector is responsible to inspect an average of 3,500 units every year.

Funding and Fees

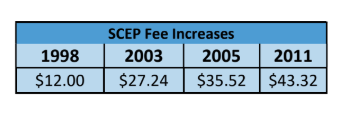

SCEP is supported by a per unit annual assessment on all property owners of rental residential complexes with two or more units. Landlords are allowed to pass on the SCEP fee to their tenants which amounts to $43.32 per unit per year. As required by the Los Angeles Municipal Code, the fee is paid annually although inspections are done on a periodic basis. The fee is intended to cover the costs of the periodic inspection and one re-inspection to ensure cited violations have been corrected. Any additional re- inspections are charged to the owner at $201 per inspection.

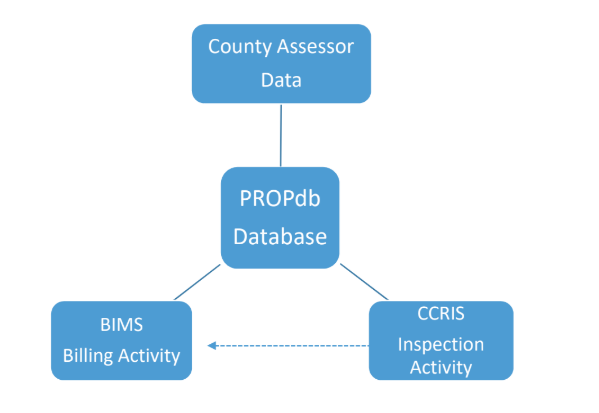

Key HCID Systems

As previously noted, the County’s Property Tax database is the primary source of property information to identify residential rental properties subject to SCEP. The County’s data is filtered for specific land use codes and unit counts to populate HCID’s PROPdb. The PROPdb acts as the Department’s centralized property data system that is relied on to identify properties to be inspected and billed the annual SCEP fee. PROPdb acts as an umbrella database that feeds into HCID’s subsystems – the Billing Information Management System (BIMS) and the Code Compliance and Rent Information System (CCRIS).

Implemented in 2008, BIMS is used to track all of HCID’s billing activity, including all properties that are exempted from SCEP and the Rent Stabilization Ordinance (RSO)7. BIMS also contains historical customer information and property ownership data. BIMS is used to issue bills to property owners and provides efficiencies for both Billings and Collections Unit and Code Enforcement staff. For example, BIMS automatically generates delinquent fee letters to Owners if payments have not been received. The system also interfaces with CCRIS, and automatically generates bills for re-inspection fees if one is required.

CCRIS was developed in 2005 and maintains relevant inspection information for all of the properties subject to SCEP. It is used to schedule inspections and document inspectors’ notes. Inspectors use F5 tablets in the field to document inspection findings and take photos. CCRIS is updated in almost real time from F5 data.

7 The Rent Stabilization Ordinance (RSO) was adopted in 1979 in order to safeguard tenants from arbitrary rent increases while providing landlords with just and reasonable returns from their rental units.

The diagram below shows the relationship between the key various County and HCID systems (there are other City systems that combine data or help identify newly constructed properties).

Billings and Exemptions

The Billings and Collections Unit (BCU) is responsible for issuing bills to the properties that are listed in PROPdb and have been determined to be subject to the provisions of SCEP and/or RSO. BCU also oversees the outside agencies that pursue collection of outstanding fees on the Department’s behalf. Uncollected accounts are referred to collection agencies after HCID has been unsuccessful in collecting outstanding fees after two delinquent notices.

During the last week of December or first week of January, BCU sends the annual billing package to owners that includes an invoice for the current year fees, exemption applications, rent register forms and other information. Property owners are to submit their exemption applications by January 31. The following table summarizes the total number of properties billed and those that were exempt from SCEP regulations and fees for the previous five years:

Despite new properties and units being built and added to the SCEP database, properties are also being deleted from the database as not being subject to SCEP enforcement and inspections.

HCID’s Systematic Code Enforcement Trust Fund

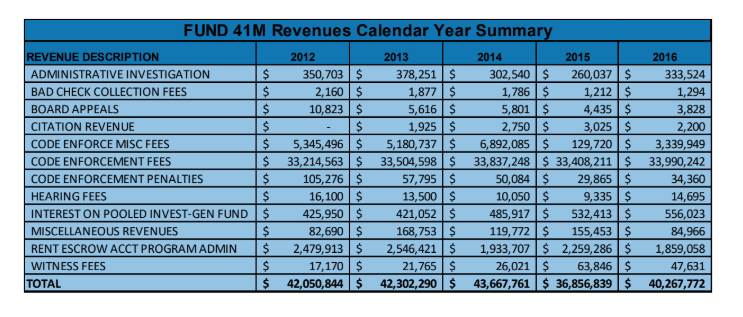

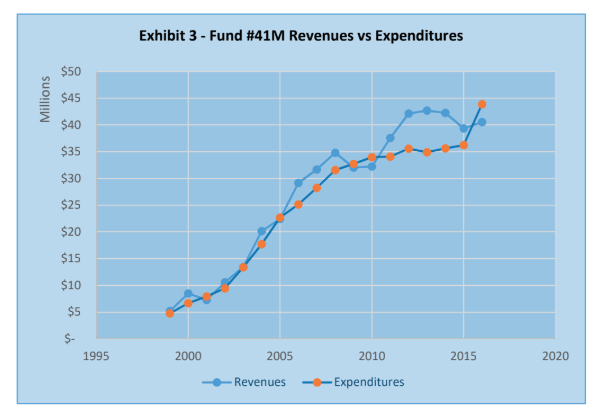

As received, the SCEP Inspection fees are credited to the Systematic Code Enforcement Trust Fund (#41M), a special revenue fund managed by HCID. Over the last five fiscal years, annual revenues for the Systematic Code Enforcement Trust Fund have averaged $41 million, while expenditures have averaged $37 million. Except for 2016, the revenues have outpaced expenditures, and the Fund’s cash balance has increased since 1999, to $54 million as of our audit fieldwork8. The Systematic Code Enforcement Trust Fund is used solely for SCEP related revenues, including late fees and fees assessed for hearings. The table below notes the revenue classifications and related amounts credited to the Fund from 2012 through 2016.

8 Cash balance as of December 2017 was $34 million.

For SCEP to remain sustainable, HCID must ensure that SCEP fees are billed and collected only for those properties that are subject to the required inspections and enforcement. Doing so ensures SCEP’s long-term viability and public support.

While there may be instances of billing properties that are not subject to SCEP regulations, such errors should be infrequent and quickly corrected. HCID must also maintain accurate and complete property records for scheduling inspections and billing purposes. Billing records should be accurate to reasonably ensure that the City only collects the fees it is entitled. Monies collected in error should be refunded quickly. Our audit identified areas where HCID can make improvements in its billing practices, fee exemption approvals, refund processes and updates to its PROPdb.

Finding #1:

The Department has billed and collected fees for properties that were not subject to SCEP.

Discussion

Land use codes identify properties that are subject to SCEP and generally serve as the identifier to initiate the annual SCEP billings. Of the more than 120 land use codes recorded by the County, only 57 meet the criteria for SCEP regulations.

However, the County codes do not translate perfectly to all buildings subject to SCEP. Sometimes, the County’s assigned land use code is incorrect and HCID applies a secondary land use code in CCRIS. The actual property use may be identified by a SCEP Inspector through a site visit. The corrected information should be noted in CCRIS, reviewed by the inspector’s supervisor and forwarded on to inventory management for investigation and final determination. In other cases, incorrect land use codes or other issues may be identified by HCID’s working group of Code Enforcement, BCU, and Rent Stabilization Unit and System Division staff. The working group was created by HCID in order to address database issues. Since 2008, the working group meets periodically to review the PROPdb file that is used for billing SCEP and RSO fees to owners. Lastly, a property owner may notify HCID that their property is exempt after receiving the annual bill. Inventory management staff must then investigate and make a final determination if the property is or is not subject SCEP and update the system.

Regardless, CCRIS as HCID’s system of record, should be updated with correct land use codes to ensure PROPdb’s billing file is accurate, and only properties subject to SCEP are billed the annual fee assessment.

During the course of the audit, we identified the Department’s billing process does not adequately ensure that only properties subject to SCEP are billed; in addition relevant information regarding whether a property is subject to SCEP is not effectively communicated to ensure that only properties that are subject to inspection are assessed SCEP fees.

We noted that BCU’s general practice is to bill if the property is listed with more than one unit, or the property owner paid the prior year’s billing.

We analyzed billing data files for calendar years 2012-16 and identified that 1,697 properties were billed in error, totaling $2.7 million, of which property owners actually paid $743,776. BCU acknowledged there were billing errors due to their processes as well as other factors such as incorrect land use codes from the County’s database. Auditors observed that the Department has been working to correct its billing errors, especially in its 2017 billing file.

We also noted that when staff discover billing or land use errors, the information is not always effectively communicated. Specifically,

Inspectors’ comments in CCRIS regarding a property’s land use were not always reviewed by supervisors and forwarded on to inventory management staff for a final determination as, to whether the property was subject to SCEP; and

BCU does not always notify inventory management staff of owners’ complaints that they are not subject to SCEP. While BCU annotates this information in BIMS, it does not always notify inventory management to investigate and make the final determination. We noted one case where the property owner has called multiple times since 2009 indicating that their property was not located in the City. BCU continued to bill the property owner and sent the account to collections. In November 2016, with the owner threatening a lawsuit, BCU staff formally notified inventory management staff, who then determined the property was not subject to SCEP and removed it from HCID’s inventory.

The above conditions existed for a variety of reasons.First,HCID did not minimize billing errors by applying appropriate data filters to exclude properties that are unquestionably exempt from SCEP (e.g. condominiums, single-family residences, stores, etc.). We analyzed SCEP billing data files used four years (2012 through 2016), and noted 67 land use codes associated with 1,697 properties that did not meet the criteria for multifamily rental properties. For example, we identified condominiums and mobile homes that were included in the property database, though SCEP does not apply to either. Because the property records indicated two or more units, they remained in the database.

Second,HCID did not have a reliable process to ensure incorrect land use codes identified by inspectors or owners are effectively investigated and corrected in CCRIS before billing. We noted some cases where the inspector’s comments noted within CCRIS regarding a property’s land use were not reviewed by supervisors and forwarded on to inventory management for final determination. For example, in 2009 an inspector included a note in CCRIS that a property was exempt from SCEP because it was actually two commercial buildings. However, CCRIS was not corrected and HCID continued to bill the owner and schedule the property for inspections. In 2013 and 2016, inspectors again noted the property was two commercial buildings. The property owner paid the City $9,573 since 2006. While BCU credited the owner’s account, auditors noted a refund had not been issued (see Finding #3).

Third, some properties have an incorrect land use code from the County Assessor’s records, and HCID’s secondary land use code was not updated in CCRIS. We noted an example where an inspector identified a property as a “condo-multifamily” in December 2013. CCRIS contained notes that this was discussed with the inspector’s supervisor; however, the land use code was not changed, and the property remained in the inventory records for 2014 and 2015. RSO and SCEP fees were billed to the property owner but only the RSO fee had been refunded. In another example, an inspector noted in CCRIS a “home for the aged” property was a state-licensed drug treatment facility. This notation was made in 2009, however, the land use code was not changed; the property remained in the inventory records, and was scheduled for inspections in 2013 and 2016. As a result of our review, the secondary land use codes for these two properties were updated in CCRIS.

Fourth, CCRIS includes some properties with land use codes that may or may not be subject to SCEP, such as “home for the aged” and “store and residential combination.” “Home for the aged” can include properties that are multifamily rental units for senior citizens (SCEP applies) as well as State-licensed community care facilities, also known as assisted living facilities (SCEP does not apply). Store and residential combination buildings have commercial enterprises at the street level with apartments above (SCEP applies) or, with condominiums above (SCEP does not apply).

While HCID’s working group identifies billing issues and works to the appropriately resolve them, we noted the group does not formally document its decisions on which land use codes should be changed or included in the billing file.

HCID management had previously identified some of the problems noted and created a new inventory management function in 2012 with one part-time employee. In December 2015, management assigned one full-time Sr. Inspector to inventory management to review and research unit count discrepancies and to determine if a property is subject to SCEP. HCID management indicated that since this function is relatively new, some staff do not forward documentation for properties that require investigation and determination. The inventory management staff have been reviewing the PROPdb to identify any properties that require a land use determination. We noted progress in this area in more recent data; the 2016 HCID billing data file contained fewer land use codes that were not subject to SCEP.

During field work, we suggested to Code Enforcement management that the newly enhanced CCRIS “2.0” should alert the inventory management unit when the property/unit may not be subject to SCEP. Subsequently, we learned the system contractor was requested to add this function to the new system which will send an alert with the property information to inventory management staff for further investigation and determination. As CCRIS 2.0 is developed, management should ensure it is capable of alerting inventory management of inspectors’ notes on a property’s land use code. HCID indicated that CCRIS 2.0 will be launched by the end of 2018.

Recommendations

HCID management should:

1.1 Enhance the internal controls as necessary to ensure that only properties subject to the SCEP fee are billed, for example by:

ensuring its systems recognize only those land use codes that meet SCEP regulations, and

investigating properties that are found to be exempt and noting the final determination in CCRIS property records.

1.2 Ensure that the new CCRIS 2.0 is capable of automatically alerting inventory management properties that require further investigation and determination based on an Inspector’s notes.

Finding #2:

The Department does not effectively administer SCEP fee exemptions. In some cases, property owners filed applications for exemptions, but when the exemption expired the SCEP billings continued prompting some owners to pay fees that were not refunded.

In addition, when an exemption expires in BIMS, the properties automatically return to the SCEP inspection inventory. However, this wastes resources because it dispatches inspectors to properties/units that are not subject to inspection.

Discussion

The Department has established three types of exemptions from the SCEP requirements and related fees: permanent, conditional and temporary which owners can apply for depending on their situation.

HCID’s data shows that an average of 15,000 properties are fully exempt (i.e., all units were excluded from SCEP inspections and fees) and an additional 20,000 properties were partially exempt, where one or more units did not require fees or inspection but others did.

Permanent Exemption

A permanent exemption application is granted for properties that are not multifamily rental properties, such as single-family residences, condominiums, mobile homes, commercial buildings, etc., or if a property is located outside of the City’s jurisdiction.

Conditional Exemption

Conditional exemptions are in effect for three years and are granted for properties where the current use of the property is exempt from SCEP, but the use could change to one that is covered by SCEP. Properties with conditional exemptions include: commercial use buildings; demolished property; monasteries, convents, or on-campus dormitories; units withdrawn from the rental housing market; hospitals or licensed care facilities; co-ops with regulatory agreements; fraternity or sorority houses or off-campus dorms; condominiums; government owned or managed buildings; and mobile home parks.

Temporary (Annual) Exemption

A temporary exemption is granted if one or more units are owner-occupied or vacant, and no rent is collected or due. The exemption is considered temporary because the property’s use is subject to change (e.g., the owner may move out and rent the unit). This exemption must be renewed and approved annually. The initial application requires the owner to submit a notarized affidavit; subsequent annual applications can be submitted indefinitely. Temporary exemptions are approved by HCID based on the owner’s self- certification.

Exemption applications are mailed out with the annual billing packet in December/January, and they can also be downloaded from HCID’s website. These applications must be submitted by January 31. Temporary exemptions may be renewed online, but conditional and permanent exemption applications must be mailed to HCID. HCID staff are expected to process thousands of exemption applications before February 28, since BIMS may assess a late penalty to owners that did not pay the full amount of their bill by that date.

During the course of the audit, we found that HCID’s exemption application process has led to owners being billed SCEP fees for properties that are not subject to SCEP; in some cases, the fees were paid but the monies have not been refunded.

This was made evident to us by two distinct conditions.

First, we observed that many properties were exempted for many years, but the Department kept billing them. We selected a sample of permanent, conditional and temporary exemptions from 2012-2016 to determine whether the exemption status was properly supported and processed, which should have prevented the owner from being unnecessarily billed. We noted:

4 of 10 (40%) permanent exemptions reviewed had $61,000 billed and collected and the monies had not been refunded to the property owners since 2014-2015. In addition, the Department did not have the owners’ documents requesting a permanent exemption for 8 of 10 exemptions reviewed.

4 of 5 (80%) conditional exemptions were properties coded as “home for the aged” and were determined to be state-licensed care facilities that are exempt from SCEP. The remaining conditional exemption was for a property being used as a monastery. However, only two of the five properties had the owner’s exemption documents uploaded to HCID’s billing system, BIMS. In addition, three of the five properties had initially requested a conditional exemption in 2005 and 2009. We also noted that the University of Southern California (USC) and University of California, Los Angeles (UCLA) have filed conditional exemption applications for several buildings used by fraternities for decades. Extending the expiration date for properties that do not frequently change use would help reduce the number of bills sent out, reduce the inventory of properties scheduled for inspections, and potentially reduce the need to refund incorrectly paid fees.

6 of 20 (30%) properties that applied for a temporary exemption had all their units exempted, and did not have a record of a single payment in BIMs since 2005. However, BCU continued billing these owners every year. Approving exemptions before SCEP billings are prepared would reduce the number of bills mailed, prevent collecting more inspection fees than the City is entitled to, and relieve owners from having to request refunds.

Second, auditors found BCU processes lacking:

First, BCU staff did not process some temporary exemption requests in BIMS. We received a list of 139 property owners who requested an exemption and had paid their bill in full, and observed staff notes for 45 of these properties that the exemption was not processed to avoid creating a credit.

To verify this information, auditors selected a sample of 10 properties and found 9 exemption requests were not approved in BIMS. These 10 property owners were assessed inspection fees for a total of 20 units, but inspections were done only in 10 units because the remaining units were owner-occupied according to inspectors’ notes. However, since the exemption requests were not completely processed, property owners still paid the inspection fees for units that were not subject to SCEP. Further, unless the owners request a refund, these monies will remain in the Trust Fund balance.

Second, when the exemption is approved and recorded in BIMS, a credit is created in the customer account. However, despite approving the exemption and recording a credit (an amount due the property owner), the Department does not notify the owners or automatically start the refund process. In fact, these property owners will be billed the full amount for SCEP fees on the next annual assessment, without an offset of the money previously due to them. Since the owners do not know that their exemption applications were approved or that they have a credit in their accounts, the owners are likely to pay the full amount again.

The above conditions existed for various reasons.BCU’s billing practice is to mail exemption forms along with the annual bill. If an exemption is approved, the SCEP fees should be less, or not billed at all. However, this practice does not ensure property owners have enough time to file for an exemption prior to the SCEP deadline; thus, many owners pay the full amount of their annual billing and at the same time they apply for an exemption, to avoid penalties if the exemption is denied. Further, since the Department does not notify the owners when the exemptions are approved, owners are unaware of any account credits. BCU management indicated that sending out exemption forms separately would be complicated and that the City would expend additional resources in postage. However, if HCID approved exemption applications prior to billing property owners, BCU management can reduce the total number of billings mailed which would reduce the postage expenditures.

BCU has not examined its database to identify properties that have had all the units exempted for five years, ten years, or more. These properties could be sent an exemption form prior to the start of the inspection cycle so that HCID could determine if the property remains exempt, or if it should be scheduled for inspection and included in the annual SCEP billing.

Recommendations

HCID management should:

2.1 Perform a cost analysis to consider sending exemption forms to property owners prior to mailing SCEP billings so that approved exemptions are reflected in the amount billed, or the need for a bill is eliminated.

2.2 Identify properties that have approved conditional exemptions for many years and determine whether the conditional exemption period should be extended beyond three years. This would enable universities and colleges, and other property types that are less likely to change their land use, to submit exemption forms on a less frequent basis.

2.3 In conjunction with Recommendation 1.1, properties used as State-licensed facilities should be identified and confirmed as having a current and valid license through the State’s licensing website in order to exclude these properties from the billing file and scheduled inspections.

Finding #3:

The Department’s refund process does not adequately ensure that monies are returned to property owners. As of April 2017, more than 17,000 properties had credit balances that totaled $2.9 million, which should be refunded. HCID reported that its liability (the money owed) was $1.3 million for the Systematic Code Enforcement Trust Fund; therefore, the City appears to have an understated liability by at least $1.6 million.

Discussion

HCID bills approximately 111,000 properties every calendar year. Refunds of SCEP fees may occur if:

Duplicate payments are received (e.g., the property owner and the property Management Company both pay SCEP fees for the same property).

The property owner pays SCEP fees before an exemption application is approved.

The City erroneously billed the property owner.

Property owners can download the Claim for Refund Application form from HCID’s website. The Claim, with proof of payment and supporting documentation as to why a refund is due, must be mailed to HCID within one year from the date of payment. The Department adheres to Los Angeles Administrative Code Section 5.170 which states that “…. All claims relating to any other causes of action shall be presented not later than one (1) year after the accrual of the cause of action.”

Upon submission, HCID’s Accounting Division reviews all the required documents, posts the liability to the Customer Overpayment Liability account in the City’s Financial Management System (FMS), and initiates a refund check to the payer.

During the course of the audit, we found that HCID management does not have adequate internal controls to ensure customers’ refunds are processed timely and that the total liability is known. The Standards for Internal Control in the Federal Government published by the United States Government Accountability Office, 9 states that “management should design control activities to achieve objectives and respond to risks”. Further, management should use quality information to achieve its objectives. In that regard, HCID could do more to minimize the amount of outstanding credits and refunds due to owners. This was made evident to us by three distinct conditions:

First, according to HCID’s Accounting Division records, 1,017 refund requests approximately $700,000 were received from FY 2014 through FY 2016; however, only 652 requests for $445,967 were shown as approved refunds, and 195 were denied. The remaining 170 requests were either not processed or were still in process according to staff notes.

Second, the total amount of refunds due owners was not accurately reflected in the Trust Fund’s liability account. As of April 12, 2017, BIMS had 17,480 properties with credit balances that totaled $2.9 million; however, the corresponding balance on the City’s Financial Management System (FMS) for Customer Overpayment Payable was $1.3 million. Therefore, the City had an understated liability of at least $1.6 million, despite HCID staff in various divisions being aware that properties were billed and paid in error. It is imperative that management record accurate information on FMS, since it is the basis for the City’s Comprehensive Annual Financial Report which reports the City’s financial status to its stakeholders.

Third, we noted that some refunds were not processed due to a lack of action by one of the responsible divisions. For example, Accounting’s refund records noted that requests could not be processed until BCU adjusted the account in BIMS. We also found that Division Managers outside of the Accounting Division do not believe that their staff are responsible to initiate the refund process even when they identified that the property owner was billed by error. Code Enforcement management indicated that the inspectors are only responsible for inspections and BCU management stated its staff does not notify the Accounting Division of refund requests, because BIMS produces a monthly report that shows accounts that were adjusted during the month. However, the Accounting Division only uses the report’s totals to post adjusting entries to FMS, and does not act on individual accounts.

9 The Standards for Internal Control in the Federal Government are based upon the 2013 Internal Control – Integrated Framework published by the Committee of Sponsoring Organizations (COSO). This framework is generally considered to be the standard bearer for providing principles for the establishment of an effective internal control system for any entity, regardless of the industry it is in and regardless of whether that entity is in the public or private sector.

The above conditions existed for a variety of reasons. The Accounting Division did not consistently use BIMS to annotate in the owner’s account why the refund request was denied or what was delaying the final disposition. Instead, the Accounting Division’s current practice is to notify the property owners about their refund request through emails and phone calls; notes are then made on the refund request spreadsheet. Without documenting reasons for denial (or what is preventing the final disposition) in the centralized billing system, HCID lacks adequate official records of the refund requests.

In addition, refunds are only initiated if a property owner requests a refund and the request is filed within one year of the payment date. Yet, there are instances where HCID has identified an overpayment, and it could refund or credit the property owner’s account, which would minimize the outstanding liability account balance.

As noted in Finding #2, to avoid potential penalties, some owners pay the full amount of their annual billing at the same time they apply for an exemption. When the exemption is approved, BIMS creates a credit on the owner’s account. However, HCID neither initiates the refund process, nor notifies the property owners, nor includes the credit balances in the next billing to offset the amount due. As a result, owners may continue paying fees, even when they have a credit.

Based on Accounting Division’s refund log, we noted 13 refund requests totaling $6,113 that were denied due to the one-year deadline. Although relatively small, the amounts associated with these denied refund requests will not be returned to the payors and needs to be resolved in some way. HCID has indicated that determining who to return the money is problematic if there has been an ownership change, or if the inspection fees had been passed to tenants. The City Attorney should be consulted to determine the proper disposition of these monies.

The Accounting Division indicated that between April 2015 and April 2016, HCID did refund 3,689 property owners that had credit balances totaling $287,308; however, this was a one-time project and HCID did not continue its efforts.

Recommendations

HCID management should:

3.1 Confirm the accuracy of the Customer Overpayment Liability account, including identifying the amount of monies that cannot be returned to payors, and consult with City Attorney on the appropriate resolution of these monies.

3.2 Ensure that all refund requests received and processed are documented in BIMS.

3.3 Establish a process whereby paid fees are refunded or credited to a property owner’s account when HCID staff discovers that the property was billed by error, without requiring the owner to submit a Request of Refund Application.

3.4 Establish a “lead division” to monitor the refund process and ensure responsible divisions take timely actions.

Finding #4:

The Systematic Code Enforcement Trust Fund has accumulated large cash balances, indicating that the revenues collected were significantly more than HCID’s historical costs incurred for the program.

Discussion

The City’s Revenue Policy indicates that “sufficient user charges and fees shall be pursued and levied to support the full cost of operations for which fees are charged, including all operations (direct and indirect) and capital costs. All user charges and fees for the City shall be monitored annually to determine that rates are adequate and each source is maximized…” Further, departments are expected to prepare schedules comparing actual revenue with budget amounts for periodic review by management. Management should address significant differences between budget and actual revenue.

SCEP was established under the premise that the program would support itself. Annual fee assessments on all multifamily rental properties are intended to cover costs associated with the administration and enforcement of SCEP and complaint inspections, specifically for an initial inspection and one re-inspection for each unit on a defined, cyclical basis. Receipts from the annual assessments are deposited into the City Treasury and credited to the Systematic Code Enforcement Trust Fund (#41M), a special revenue fund managed by HCID. The annual assessments are due by the end of February, but since the City operates on a 12-month fiscal year starting July 1, the City’s General Fund fronts the budgeted operational costs of SCEP with an appropriation based on estimated program expenditures. The General Fund is then reimbursed from the Systematic Code Enforcement Trust Fund on a monthly basis.

During the course of the audit, we found that the Systematic Code Enforcement Trust Fund balance has generally increased since 1999. The Trust Fund’s cash balance totaled $54 million as our audit fieldwork (April 2017); and $7.2 million of that balance was held in three liability accounts10 for monies to be refunded/returned to individuals.

The following graph shows how the Fund’s cash balance has been increasing.

HCID has increased the SCEP fee three times since 1998. Owners currently pay $43.32 per unit annually.

10 Customer Overpayment Payable $1.3 million, REAP Escrowed Rents $5.8 million and Revenue Collected in Advance $100,000.

There is a correlation between the fee increases and the increased cash balance in the Fund. Exhibit 3 shows the relationship between revenue and expenditures over time. The Fund’s annual revenues have generally outpaced expenditures, which has contributed to the increase in the Fund’s cash balance. Over the last five years, revenues for the Fund have averaged $41 million, while expenditures have averaged $37 million.

The above condition existed for a variety of reasons. We noted that the budgeted amount for program expenditures was based on salaries for the number of authorized positions, adjusted for a 5% vacancy rate (per the CAO’s recommendations). However, HCID’s vacancy rate has averaged 10% for the Code Enforcement Division for the past 11 years, and was 35% for the Billing and Collection Unit in 2016. As a result, actual expenditures have been less than budget. Further, HCID has not been able to complete scheduled inspections within the anticipated cycle time. To more accurately identify the costs that must be covered, the Program’s budgeted expenditures should be more aligned to actual costs and consider the projected number of inspections expected to be completed, annually.

We also found that unneeded appropriations and encumbrances were not consistently reversed at year-end. During our field work, in November 2016, HCID requested the Controller’s Office to reverse its prior years’ unneeded appropriations, which totaled $138 million for Fiscal Years 2010 through 2016. Although there is no City requirement for Departments to reverse unused appropriation balances or unneeded encumbrances for special revenue funds under their control, doing so would improve fiscal management of those funds and their related programs. Going forward, HCID should request the Controller to reverse any remaining appropriation balances at fiscal year-end, and revert unneeded encumbrances in a timely fashion. This will allow HCID to identify all program funding available for SCEP activities, and facilitate comparisons of actual expenditures to those proposed, to enhance program planning and financial reporting.

Lastly, as discussed in Finding #1, issues with HCID’s billing process led to collecting inspection fees for properties that were not subject to SCEP, which should be refunded and not used to cover future program costs.

Recommendations

HCID management should:

4.1 Monitor the Systematic Code Enforcement Trust Fund balance to ensure it is closely aligned with SCEP expenditures.

4.2 Prepare the SCEP budget based on a historical average of actual expenditures, taking in consideration the actual job vacancy rates.

4.3 Ensure that appropriation balances are reversed annually, and that unneeded encumbrances are reverted in a timely fashion.

Finding #5:

HCID needs to re-evaluate the fee it charges based on the new inspection cycle to ensure appropriate cost recovery of all SCEP activities.

Discussion

For fee-based programs, fees should be just enough to cover the program’s actual costs. Section 66014 of the California Government Code requires that fees charged by a local agency may not exceed the estimated reasonable cost of providing the service for which the fee is charged. If the fees or service charges create revenues in excess of actual cost, the excess should be used to reduce the fees or service charge creating the excess.

SCEP fees finance the costs of inspection and enforcement by the Department in accordance with the LAMC.11 Based on our review, the Department has adequate internal controls to ensure SCEP revenue, expenditures and inter-fund transfers are properly recorded and approved according to applicable ordinances, policies, and laws.

During the course of the audit, however, we found that HCID should revise its methodology to set SCEP fees to ensure they are based on fully recovering the direct and indirect costs of SCEP programs/activities and the actual work performed. The methodology should consider the recently implemented two-tier inspection cycle.

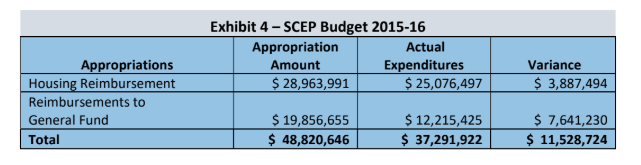

We found that HCID set SCEP fees based on budget projections to complete inspections of all multifamily rental units over a three-year cycle. However, budgeted vacancy rates (as recommended by the CAO) and anticipated inspection activity were used in determining costs instead of the actual staffing rates and actual activities completed. Generally, the amounts budgeted for SCEP activities have been higher than the actual expenditures. For example, the budgeted appropriations to fund SCEP through the Systematic Code Enforcement Trust Fund exceeded expenditures by $11.5 million, shown in Exhibit 4 below.

Further, in developing the inspection fee, HCID needs to compare the costs incurred to the number of units inspected. In the past, HCID considered the total number of units to be inspected over its inspection cycle. Also, over time, there have been more services and sub-programs that have been added to SCEP activities and inspectors’ workload. For example, SCEP inspectors also assist with the:

11 Los Angeles Municipal Code, Division 3.5, Section 161.352.

Tenant Habitability Review Plan, which protects tenants from unlawful eviction or displacement during housing remodels.

Urgent Repair Program, which handles referrals of imminent hazards.

Court Liaison Unit, which provides expert code enforcement testimony at General Manager Hearings and cases referred to the City Attorney’s Office.

Gateway to Green (G2G) Program, which partners with the Department of Water and Power to help reduce energy and water use by disseminating information regarding incentives and rebates during inspections.

HCID’s fee development review should consider all of the services and sub-programs associated with SCEP, as well as consider that Cost Allocation Plan (CAP) 12 rates have been increasing, which impacts the full costs to be recovered. In September 2015, the Controller’s Office issued the citywide indirect costs rates for CAP 37; and the Code Enforcement Division’s CAP rate increased from 36.14% to 60.36%.

The above conditions existed for two primary reasons.HCID staff has not used its Cost Allocation System to identify all SCEP-related costs for each program activity, or the actual workload completed to develop the inspection fees. The Cost Allocation System captures costs through work orders that are used by staff to record their time worked, as well as non-labor costs such as supplies. Utilizing HCID’s Cost Allocation System will ensure costs associated with all related SCEP activities are used to develop the inspection fees.

In addition, HCID did not have a data system solution to identify a baseline for inspection productivity. According to Code Enforcement management, the new CCRIS 2.0 will make it possible to determine a productivity baseline and compare it to actual performance. The system development contractor has designed a new scheduling application that will consider the building size, number of inspections and re-inspections, and the related time.

Given the recent and forthcoming changes to services provided, inspection cycles, CAP rates, and data capture, it is critical that the Department re-examine the process to develop its SCEP inspection fees.

12 Related costs include employee fringe benefits and central services costs that the City pays for in advance with the General Fund which need to be reimbursed by the Department. Accounting staff apply the corresponding Cost Allocation Program (CAP) rate to determine the amount.

Recommendations

HCID management should:

5.1 Examine all SCEP activities and sub-programs to ensure all appropriate costs are considered for inclusion in the SCEP fee. Use its Cost Allocation System to capture all direct and indirect costs associated with SCEP program activities.

5.2 Develop the SCEP fee by considering the actual program costs and the number of units actually inspected, as well as the most recent CAP rates.

To help ensure rental properties are adequately maintained, and serious problems are properly addressed, HCID developed two pilot programs to enhance the effectiveness of SCEP. These new programs: 1) modify the complaint process and require inspectors to observe alleged violations before sending owners a notice, and 2) enable owners with a history of recurring code violations to work with SCEP inspectors to obtain guidance on how to make quality repairs. The intent of these new programs is to ensure quality repairs and reduce recurring code violations, while testing whether new procedures are effective. In addition, improving timeliness to respond to complaints can help to improve SCEP operations. These findings are discussed below.

Finding #6:

There has been little to no participation in the Pre-Inspection/Pre-Repair pilot program in its first months of implementation.

Discussion

In April 2015, due to growing concerns about the number of repeat offenders of the Housing Code, the City Council instructed 13 HCID to report on the feasibility of strengthening the Systemic Code Enforcement Program by developing an enhanced repair program, along with recommendations on what would trigger the need to implement such enhanced repairs.

Subsequently, HCID recommended two six-month pilot programs in limited geographical areas: (1) An Enhanced Repair Program which modified the complaint inspection procedures for the Central and East Regional Offices; and (2) A Pre-Inspection/Pre-Repair Conference Program in the City’s federally designated Los Angeles Promise Zone-Hollywood to provide education and outreach to owners. HCID reported that these programs would have a greater potential to improve the quality of repairs and reduce recurring code violations.

On March 22, 2016, the City Council approved the two pilot programs, but extended the time period from six months to twelve months.

13 On April 17, 2015 Council Member Gilbert Cedillo (CD 1) introduced a motion (CF: 15-0463)

Enhanced Repair Program

Previously, owners could make superficial repairs to address issues noted, and SCEP inspectors could not determine the underlying cause of the problem, resulting in recurring code violation(s). In September 2016, HCID implemented the Enhanced Repair pilot program. The pilot program modified HCID’s complaint inspection procedures by having inspectors meet with the tenant/complainant first, instead of sending a courtesy notice to the owner to correct the problem. The inspector can now verify the reported problem, identify the underlying causes, and give the property owner a 30-day notice explaining how to correct the problem. If the condition is not corrected, the letter is upgraded to an Order to Comply.

Pre-Inspection/Pre-Repair Conference Program

In December 2016, HCID implemented the 12-month pilot program to establish a pre- inspection/repair conference program to provide guidance to owners whose properties are scheduled for a SCEP inspection. This program reaches out to owners/agents with properties that have a history of violations and provides education on how to make quality repairs. A notice of pre-inspection conference is sent along with the notice of initial SCEP inspection. Owners can then call a senior inspector to schedule a pre- inspection conference before the initial inspection. Similarly, if an inspection notes a problem and an order to comply is issued, a notice of a pre-repair conference is sent along with the order. Both conferences are currently held at the Central regional office.

The purpose of this pilot program is to the test different processes to determine its success before expanding to a wider population.

In the course of our audit, we found that property owners are not taking advantage of the Pre-Inspection/Pre-Repair program.

For the first 4 1⁄2 months of this program (January-April 15, 2017):

Only 3 of 559 owners who received a notice requested a Pre-Inspection conference.

There were no requests for a Pre-Repair conference out of the 604 notices sent to owners.

The above condition may have occurred for a variety of reasons. For example, these pre- conferences are optional, and owners may not be interested in meeting with the Department or owners may not be fully aware of the programs’ benefits. The Department acknowledges that the program is not working as it was intended.

While a low level of participation may occur in the early implementation of a pilot program, it is important that the Department identify the causes of low participation, when it continues. Metrics should be established to measure the success of any pilot program, which can then be used as the basis for future decisions.

Recommendations

HCID management should:

6.1 Identify the reasons for low participation in the pilot programs to identify needed changes if large-scale, or full implementation is approved.

Finding #7:

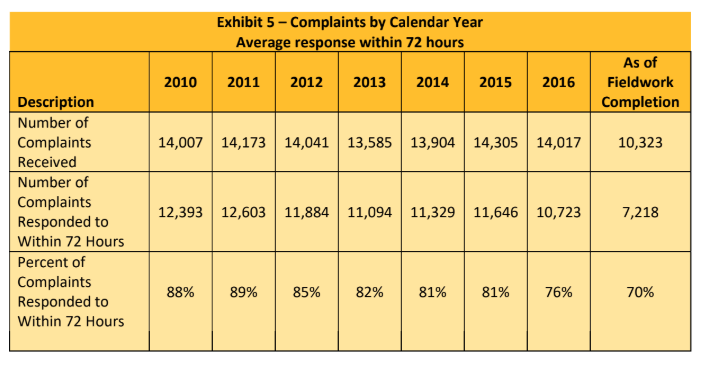

HCID responded to 70% of complaints within 72 hours of contact in 2017, a significant decrease from its historical five–year average of 83%. Moreover, HCID does not monitor the length of time to resolve complaints.

Discussion

In addition to the scheduled, proactive inspections of all units, HCID also administers the Complaint Inspection Program for residential rental units, which is a sub- component/activity of SCEP. HCID inspectors conduct inspections of properties in response to complaints filed by tenants or others. The Department’s goal is to contact the complainant within 72 hours, which initiates HCID’s process of investigation, inspection and resolution.

Complaints are classified as two types:

Urgent: Any condition that poses a serious risk or immediate hazard to the health or safety of the occupants or the public. Examples include no heat during winter or illegal construction.

Non-Urgent: Examples include leaky faucets, inoperable windows or peeling paint.

According to the Standards for Internal Control in the Federal Government published by the United States Government Accountability Office14 there should be top-level reviews of performance by management, where actual performance is compared to planned or expected results throughout the organization, and significant differences are analyzed.

In the course of our audit, we noted that HCID’s ability to respond to complaints within its goal of 72 hours has decreased from 83% in 2010-15 to 70% in 2017.

Moreover, HCID management did not have a performance goal for how many days it should take for a complaint to be resolved.

14 The Standards for Internal Control in the Federal Government are based upon the 2013 Internal Control – Integrated Framework published by the Committee of Sponsoring Organizations (COSO). This framework is generally considered to be the standard bearer for providing principles for the establishment of an effective internal control system for any entity, regardless of the industry it is in and regardless of whether that entity is in the public or private sector.